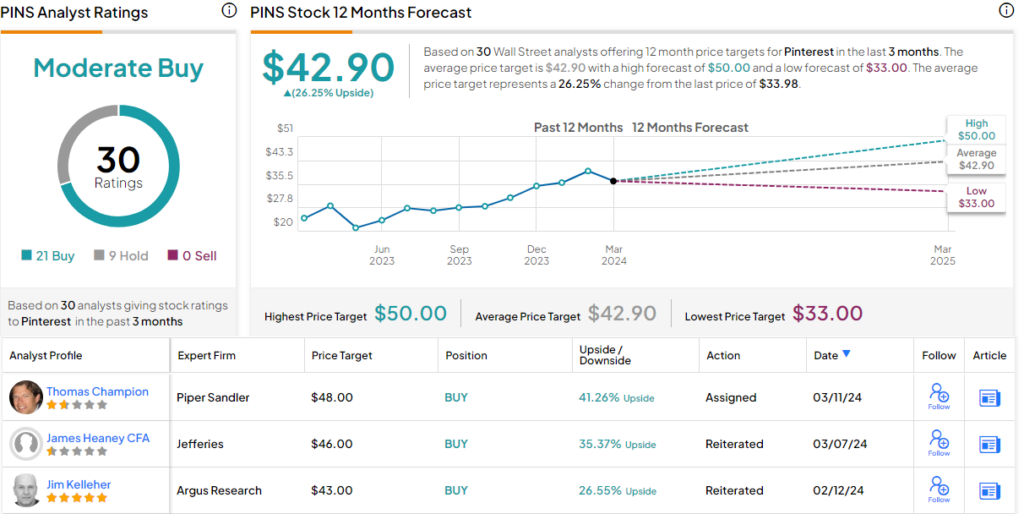

The primary quarter is sort of behind us, and analysts are beginning to discern the patterns which might be shaping the yr’s inventory markets. Two key factors are already standing out. One is the excessive ranges of market focus; the Magnificent 7 mega-cap tech corporations are nonetheless absorbing a disproportionate share of the good points. The second, associated to this, is a must diversify – however to decide on the diversification rigorously.Buyers can’t depend on a normal broadening of the market to carry a portfolio. Moderately, what’s wanted is a specific sector that may carry new alternatives by constructing on the Magazine 7s’ present good points. AI shares match this invoice.Everyone knows how AI tech is altering the digital panorama. Writing from Goldman Sachs, chief US fairness strategist David Kostin has some perception on the ways in which AI will broaden buyers’ choices via the remainder of this yr: “US fairness market focus has jumped to the best stage in a long time. Whereas anxious buyers have targeted on the DotCom bust in 2000, different concentrated markets previously 100 years typically resulted in ‘catch up’ rallies because the market broadened. Neither a ‘catch up’ nor a ‘catch down’ look very more likely to us within the near-term within the absence of a serious shift in rates of interest or a deterioration within the outlook for mega-cap earnings.”“AI has captured investor enthusiasm, however that commerce seems to be broadening,” goes on so as to add. “Shares in Part 2 (AI infrastructure) and Part 3 (AI-enabled revenues) have just lately outperformed friends, and we finally anticipate Part 4 will seize these corporations greatest positioned to get pleasure from elevated productiveness.”Following this, Goldman’s inventory analysts are telling us to ‘purchase the AI beneficiaries past the excessive momentum shares,’ and are particularly mentioning these 3 names for buyers to think about. With assist from the TipRanks database, we will additionally gauge normal Road sentiment towards these names.Pinterest (PINS)First on our Goldman-backed record is Pinterest, the visually oriented social media platform that offers customers a web-based bulletin board to show graphic content material within the on-line social universe. Pinterest follows the standard social media mannequin, with customers publishing and sharing content material, both publicly or privately. The graphic-based platform, which additionally helps video content material, lets customers kind their digital bulletin boards into classes, making it simpler for viewers to search out and browse the pages. The visible orientation of the Pinterest platform has lent itself to e-commerce, and customers can arrange their pages as on-line storefronts. Pinterest has invested closely in AI know-how, utilizing it to energy the search perform, and to kind and curate customers’ pins and posts.Story continuesAs a social platform, Pinterest skews each younger and feminine. The consumer base is roughly 60% ladies, and the 18 to 25 age demographic is the platform’s quickest rising. The corporate doesn’t explicitly market itself to younger ladies, however administration can’t keep away from catering to the platform’s largest viewers – in June of 2022, the corporate acquired THE YES, an AI on-line buying platform, for $87.6 million. The transfer expanded Pinterest’s capabilities in on-line commerce, and its enchantment to its younger and feminine core demographic.Pinterest has seen current sturdy good points in its consumer base. Within the 4Q23 report, the final launched, Pinterest reported 498 million world month-to-month lively customers (MAUs) as of December 31, 2023. This was up 11% year-over-year, and was an all-time excessive for the corporate.For the full-year 2023, Pinterest had $3.055 billion in revenues, up 9% y/y; for This autumn, the highest line of $981 million was up 12% y/y – though it missed the forecast by $9.2 million. On the backside line, Pinterest had non-GAAP earnings of 53 cents per share, a strong y/y achieve from the 29 cents reported in 4Q22, and a pair of cents per share higher than had been anticipated.All of this caught the attention of Goldman’s 5-star analyst Eric Sheridan, who took the measure of Pinterest’s actions, and got here down with a bullish viewpoint: “In our view, PINS mgmt stays targeted on constructing scale right into a wider pool of advert budgets (advertiser range, new product iteration and higher monetization of intent alerts) to drive an improved income trajectory within the quarters and years forward. When it comes to margin construction, This autumn Adj EBITDA outcomes continued to display how prior interval investments at the moment are constructing into ahead yr margin trajectory. Wanting past the short-term narratives on price of change in advert income progress charges within the coming quarters, we now have a rising confidence interval in PINS mgmt long-term initiatives (buying/commerce, depth of engagement throughout media varieties, worldwide monetization, and so on.) which might produce sustained above-industry common income progress over the subsequent 2-3 years.”Summing up, Sheridan offers PINS a Purchase ranking, with a $41 worth goal that factors towards a 20.5% achieve within the coming months. (To observe Sheridan’s observe file, click on right here)General, Pinterest has a Average Purchase ranking from the consensus of the Wall Road analysts, primarily based on 30 current evaluations with a 21 to 9 breakdown of Purchase vs Maintain. The shares are buying and selling for $33.98 and their $42.90 common worth goal is barely extra bullish than the Goldman view, suggesting a one-year upside potential of 26%. (See Pinterest’s inventory forecast)Coupang (CPNG)Subsequent on our record is the Korean e-commerce participant Coupang, a powerful market chief within the Asian nation’s on-line retail sector. Coupang goals to ‘wow’ its prospects, and provides an e-commerce platform on which prospects should buy nearly something. The corporate additionally offers dwelling supply companies, and even a web-based streaming service, Coupang Play. The breadth of services, and the assured supply, have led some to name the corporate ‘South Korea’s Amazon.’The web service is complemented by a community of bodily infrastructure, designed to facilitate the corporate’s warehousing and supply companies. Coupang has over 100 success facilities, primarily based on the Amazon mannequin, housing its merchandise and totaling greater than 47 million sq. ft. The warehouse and logistic community is dense; it’s estimated that 70% of South Korea’s inhabitants lives inside 7 miles of a Coupang facility.Together with the warehouse community, the corporate makes use of top-end software program techniques, together with AI-powered machine studying, to again up the e-commerce aspect and coordinate the bodily deliveries. The software program techniques can predict demand spikes, route merchandise into the supply community, and guarantee environment friendly dealing with of all orders, in order that prospects have extra decisions at a decrease price.In an attention-grabbing improvement, Coupang in January accomplished its acquisition of the net luxurious retailer Farfetch. Farfetch, which is predicated within the UK, offers a worldwide buyer base with entry to a variety of luxurious items. Coupang acquired the corporate for $500 million, a surge in capital for Farfetch, that may enable the corporate to proceed serving its 4-million-strong buyer base. Coupang may even make its logistic experience accessible to the brand new acquisition – and can achieve entry to Farfetch’s product traces of luxurious items and its worldwide presence.Turning to monetary outcomes, we discover that Coupang reported revenues of $6.56 billion in 4Q23, for a 23% year-over-year achieve. The quarterly prime line additionally got here in $150 million above the forecast. On the backside line, the corporate had a non-GAAP EPS of 8 cents per share, 2 cents forward of the pre-release estimates. Coupang complemented this quarterly efficiency with strong money era; for the complete yr 2023, the corporate reported $2.7 billion in working money move and $1.8 billion in free money move.Eric Cha follows Coupang for Goldman Sachs, and reiterates his perception that buyers will not be appreciative sufficient of CPNG’s advantages. He writes, “We keep our constructive view on the inventory: We word some market issues on potential overhang from promoting by giant shareholders (as seen publish prior quarterly outcomes), however we proceed to be constructive on fundamentals given Coupang’s differentiated moat driving multi-year market share achieve momentum within the home retail area. Coupled with scale-driven working leverage and GMV combine shift in the direction of extra worthwhile enterprise mannequin (i.e. FLC), we anticipate substantial scaling of FCF for the corporate, which we imagine continues to be being under-appreciated.”These feedback help Cha’s Purchase ranking right here, and his worth goal, set at $30, implies a achieve of 64.5% on the one-year horizon. (To observe Cha’s observe file, click on right here)As soon as once more, we’re taking a look at a inventory with a Average Purchase consensus ranking – this one derived from a good break up of three Buys and Holds, every. The shares have a buying and selling worth of $18.23, and the $21.10 common goal worth signifies potential for a 16% one-year upside. (See Coupang’s inventory forecast)Amazon (AMZN)Final on our record is Amazon, the 800-pound gorilla of on-line commerce. Amazon is an organization that has confirmed itself able to rolling with no matter modifications the market can throw at it. It survived the unique dot.com bubble, it has expanded far past its origin as a web-based bookstore, and it has turn out to be the biggest on-line retailer on the planet, providing an unmatched line of merchandise and buying a really world attain.Because of changing into the world’s chief in on-line retail, Amazon has additionally turn out to be one of many world’s most dear publicly traded firms. Amazon is without doubt one of the Magnificent 7 mega-cap shares, and with its $1.81 trillion market cap, it’s the fourth-largest public firm on Wall Road. Amazon’s sheer scale is seen in one other quantity, its day by day gross sales quantity of roughly $1.4 billion.Like Coupang above, Amazon has a widespread community of brick-and-mortar success facilities, warehouses, and logistic hubs to help its e-commerce enterprise. The corporate boasts that it could actually assure fast supply almost wherever on the globe, and the warehouse community is geared to offer that. A few of Amazon’s amenities have greater than 1 million sq. ft of workspace, giving the corporate a strong bodily presence that brings the net world to life.The e-commerce aspect of Amazon’s enterprise is large, and attracts some 2 billion month-to-month hits to the corporate’s web site. And attracting prospects is the bread and butter of Amazon’s enterprise, particularly when on-line retail could be seen as a lure. The corporate provides an array of extra companies, accessible on-line, that increasingly more prospects are discovering that they can’t do with out.These companies embrace cloud computing, the favored AWS that’s accessible by subscription buy, in addition to TV streaming, the Kindle ebooks, on-line gaming for all ages, dwelling automation, and even dwelling supply for on-line grocery orders. Amazon’s numerous companies all mix to satisfy a standard want, of fixing buyer issues in the actual world.Fixing these buyer issues has been profitable for Amazon. In early February, the corporate reported its outcomes for 4Q23, and confirmed $170 billion in income for the quarter. This was up 14% year-over-year, and was $3.74 billion forward of the estimates. On the backside line, Amazon generated $1 in EPS from its $10.6 billion web earnings. AWS, the cloud computing service that has confirmed so fashionable, generated $24.2 billion of the entire income, for a 13% y/y phase achieve.We’ll examine in once more with Goldman’s Eric Sheridan, who sees Amazon as a long-term inventory play, writing of the corporate, “Wanting over a multi-year timeframe, we reiterate our view that Amazon will compound a mixture of strong income trajectory with increasing margins as they ship yield/returns on a number of yr funding cycles. After buying and selling in a spread (& underperforming the broader market) for many of the previous 2-3 years, we see AMZN as nicely positioned for future outperformance as eCommerce margins proceed a trajectory of scaling over headwinds created lately and ongoing advantages from a extra environment friendly logistics community, as its promoting enterprise continues to attain scale and as AWS can nonetheless profit from a long-tailed structural progress alternative within the shifting wants of enterprise prospects (whereas producing a steadiness of progress and margins).”Following the This autumn print, Sheridan summed up his stance on the inventory with an upbeat outlook, saying, “…we proceed to see Amazon positioned as a pacesetter in all points of secular progress inside our Web protection (eCommerce, digital promoting, media consumption, aggregated subscription choices & cloud computing). In complete, each key metric that Amazon is measured in opposition to exceeded expectations and we come away from this earnings report with an elevated confidence interval in our medium/long run thesis of Amazon’s key platform drivers.”The highest-rated analyst offers AMZN a Purchase ranking, and he backs that up with a $220 worth goal suggesting a 26% share appreciation this yr.Amazon’s inventory has 41 unanimously constructive analyst evaluations, for a Sturdy Purchase consensus ranking. The common goal worth of $209.23 implies that AMZN has a one-year potential upside of $20%. (See Amazon’s inventory forecast)To search out good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Greatest Shares to Purchase, a software that unites all of TipRanks’ fairness insights.Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is extremely essential to do your personal evaluation earlier than making any funding.

Goldman Sachs Says ‘Purchase AI Beneficiaries Past the Excessive Momentum Shares’; Right here Are 3 Names to Contemplate

- Trending

- Comments

- Latest

{kind=link}