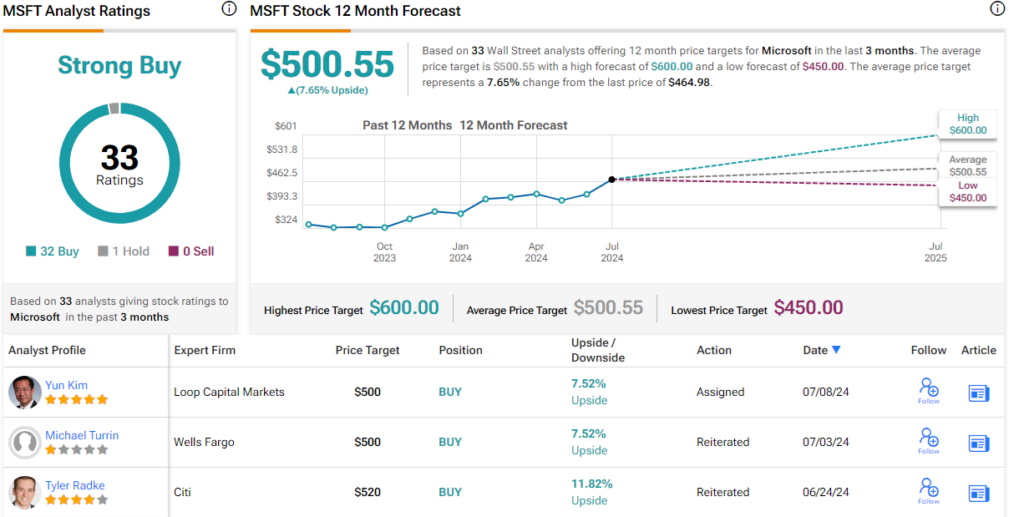

For the reason that industrial revolution of the late 1700s, know-how has knowledgeable and led a sequence of radical modifications in our societies and economies. The tempo has picked up velocity in latest many years, because the world turned digital, and now AI is powering a so-called fourth industrial revolution, primarily based on a fast trade of knowledge and knowledge.In opposition to this backdrop, tech shares have led the way in which in market features. The tech-heavy NASDAQ rose a powerful 43% final 12 months, and the S&P 500 rose 24%. Each indexes are persevering with to publish sturdy numbers this 12 months; for 2024 year-to-date, they’re up 24% and 17% respectively.This has Wedbush analyst and tech professional Daniel Ives bullish on tech shares, noting: “The primary half of 2024 has been a really sturdy run for tech shares led by Massive Tech stalwarts Nvidia, Microsoft, Amazon, Meta as this 4th Industrial Revolution has simply begun to play out in our view on this 1995 Second (not 1999) with many bears nonetheless yelling from their hibernation caves… We imagine NASDAQ has one other sturdy 2H forward as tech shares shall be up 15% the remainder of 2024 in our view with tech fundamentals set to speed up as AI use instances materially broaden.”In opposition to this backdrop, we’ve opened the TipRanks database to search for two of Ives’ inventory picks – well-known tech giants – and see how his takes stack up towards the Wall Avenue consensus. Listed here are the main points.Microsoft (MSFT)First on our checklist, Microsoft has been main the sphere in PCs and working methods for the reason that Seventies, and has turn out to be one of many world’s most iconic model names. Lately, the corporate, primarily based in Redmond, Washington, has continued its lengthy dedication to advancing know-how, by staking out a robust place at the forefront of the unreal intelligence discipline. Microsoft has a long-standing curiosity in AI, and was an early backer of OpenAI, the corporate that introduced us generative AI and Chat GPT on the finish of 2022. The corporate’s cumulative investments in OpenAI are within the neighborhood of $10 billion.From the consumer perspective, Microsoft has a number of extremely seen AI initiatives. These embrace the combination of generative AI tech into the Bing search engine, in effort to make Bing extra consumer pleasant, with an improved interface and search outcomes, aiming at a stronger competitors with Google. Additionally, Microsoft is incorporating AI into the updates for the Home windows and Workplace software program packages. Outstanding amongst these additions to the enduring software program merchandise is the Copilot, Microsoft’s new AI-powered on-line assistant. The Copilot is designed to offer real-time consumer help, knowledgeable by the consumer’s personal work and content material creation histories.Story continuesPerhaps the largest-scale use of AI in Microsoft’s product supply could be present in its cloud computing platform, the Azure subscription service. Azure is a package deal of cloud-based apps and instruments, greater than 200 all advised, and Microsoft is incorporating AI into the platform – prospects will be capable to select AI-enhanced variations of the Azure apps. The transfer guarantees to each make Azure a extra user-friendly product, with better flexibility, and to make the platform a stronger competitor to Amazon’s AWS and to Google Cloud.A take a look at Microsoft’s final monetary report, which coated fiscal 3Q24, reveals that the AI improve to Azure is bearing fruit. Azure is a part of Microsoft’s Clever Cloud phase, which generated $26.7 billion in income for the quarter, up 21% year-over-year and 43% of the quarterly prime line. The corporate’s whole income for fiscal Q3 was up 17% year-over-year, and reached $61.9 billion, beating the forecast by $1.01 billion. On the backside line, Microsoft noticed earnings of $2.94 per share, a determine that was 11 cents per share higher than had been anticipated – and was up 20% from the prior-year interval.Shares in Microsoft have proven sturdy efficiency over the previous 12 months; unsurprising given the strong monetary outcomes. The inventory has gained 42% within the final 12 months, and is up virtually 25% thus far this 12 months.For Ives, the important thing level right here is the potential of AI to unlock extra features as MSFT goes ahead. He writes, “We imagine the inventory nonetheless has but to cost in what we view as the following wave of cloud and AI progress coming to the Redmond story with a robust aggressive cloud edge vs. Amazon particularly and Google in cloud bake offs. Our latest associate checks have been incrementally sturdy round Copilot deployments with MSFT prospects and finally we estimate this might add one other ~$25 billion to Redmond’s topline trajectory by FY25. Right here is the important thing because the multiplier ripple impression from the Godfather of AI Jensen and Nvidia is simply beginning to be felt on the cloud/software program layer because the 2nd derivatives of the AI Revolution play out within the discipline.”The tech professional goes on to offer Microsoft shares an Outperform (Purchase) score, together with a value goal of $550, suggesting a one-year upside potential of 18%. (To look at Ives’ monitor file, click on right here)This venerable tech agency has picked up 33 latest analyst critiques, with a lopsided cut up of 32 Buys to 1 Maintain giving the shares a Robust Purchase consensus score. The inventory is priced at $464.98, and its $500.55 common value goal implies it can acquire 7.5% within the coming 12 months. (See MSFT inventory forecast)Salesforce.com (CRM)Subsequent up is Salesforce, a well known title within the discipline of buyer relationship administration, or CRM. Salesforce provides a superb definition of CRM, describing it as a system for managing firm interactions with all prospects, present and potential, with the easy purpose of enhancing relationships and increasing the enterprise.Salesforce has been within the CRM enterprise since 1999, and has perfected the system. The corporate gives an industry-leading, cloud-based software program platform that streamlines CRM actions, together with gross sales calls, advertising and marketing emails, and customer support interactions. The platform tracks these interactions and builds up a unified database comprised of buyer and firm data.Lately, Salesforce has built-in AI know-how into its CRM software program merchandise, additional enhancing the skills of each builders and customers to customise the platform, becoming it to any scale or enterprise function. The corporate’s AI integration streamlines knowledge retrieval, improves communications, automates repetitive duties, and generates actionable insights by means of autonomous knowledge evaluation. Salesforce can be making use of generative AI for automated artistic functions – producing personalised buyer communications, together with concentrating on advertising and marketing contacts and figuring out one of the best timing for his or her launch.Salesforce has, in its years of operation, made itself a vital a part of the enterprise universe, providing a needed service, primarily based on the newest know-how, and delivering strong outcomes for its prospects.As for Salesforce’s outcomes, the corporate reported its fiscal 1Q25 monetary launch on the finish of Could and beat the forecast on earnings whereas lacking on income. The corporate’s income got here to $9.13 billion, up virtually 11% from the prior 12 months however $20 million lower than had been anticipated. The underside line was reported as $2.44 by non-GAAP measures, for a 44% y/y improve – and beating the estimates by 7 cents per share.The corporate reported some extra metrics that ought to pique investor curiosity, together with $8.59 billion in subscription & assist income, up 12% year-over-year and a fundamental driver of the general income progress. Free money circulate was up within the quarter, by 43% y/y, to achieve $6.08 billion. Salesforce completed the quarter with $9.96 billion in money and liquid property available, as of April 30 this 12 months.Whereas these outcomes had been sound, shares in Salesforce dropped sharply after the discharge – primarily when the Q2 forecast didn’t impress. Firm estimates for each income and earnings in Q2 got here in beneath the consensus estimates. At present, the inventory is flat for the year-to-date.Dan Ives, in his protection of Salesforce, takes an investor’s perspective – and he’s impressed by the corporate’s present capabilities and near-term potential. Ives writes of Salesforce, “In our view, CRM is on the trail to a better progress, margin, and FCF trajectory and that is only a small bump within the street throughout a transitionary progress interval… CRM [remains] one among our favourite tech names to personal over the following 12 months because the AI story begins to take form. We might be consumers on weak point… as seeing the forest by means of the bushes it is a turnaround in movement for a premier tech stalwart with a large put in base led by among the best CEOs within the international tech panorama in our view.”Taking these feedback ahead, Ives charges CRM as Outperform (Purchase), with a $315 value goal that implies a 21% acquire within the months forward.There are 40 latest analyst critiques on file for Salesforce shares and so they break right down to 29 Buys, 10 Holds, and 1 Promote, giving the inventory its Average Purchase consensus score. The shares are priced at $259.81, with a $297.11 common goal value that signifies potential for a 14% upside on the one-year horizon. (See CRM inventory forecast)To seek out good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Greatest Shares to Purchase, a device that unites all of TipRanks’ fairness insights.Disclaimer: The opinions expressed on this article are solely these of the featured analyst. The content material is meant for use for informational functions solely. It is extremely essential to do your personal evaluation earlier than making any funding.

Daniel Ives Suggests 2 Tech Giants to Purchase for the Second Half of 2024

- Trending

- Comments

- Latest

{kind=link}