Folks’s ‘magic quantity’ for retirement rises quicker than inflation, leaping 15% in only a 12 months and a whopping 53% since 2020; whereas retirement financial savings falls to $88K

The ‘Silver Tsunami’ is right here: 11,000 Individuals will flip 65 every single day by 2027; solely half of Boomers+ and Gen X imagine they’re going to be financially prepared for retirement

Many years of Distinction: Gen Z began saving at 22 and expects to retire at 60; Boomers+ began saving at 37 and count on to retire at 72

Potential for Tax Planning: As tax season continues, simply 3 in 10 Individuals imagine they’ve a tax-efficient retirement plan, probably inflicting many to pay greater than required

MILWAUKEE, April 2, 2024 /PRNewswire/ — Individuals’ “magic quantity” for retirement is surging to an all-time excessive – rising a lot quicker than the speed of inflation whereas swelling greater than 50% because the onset of the pandemic. These are the newest top-level findings from Northwestern Mutual’s 2024 Planning & Progress Research, the corporate’s proprietary analysis collection that explores Individuals’ attitudes, behaviors and views throughout a broad set of points impacting their long-term monetary safety.

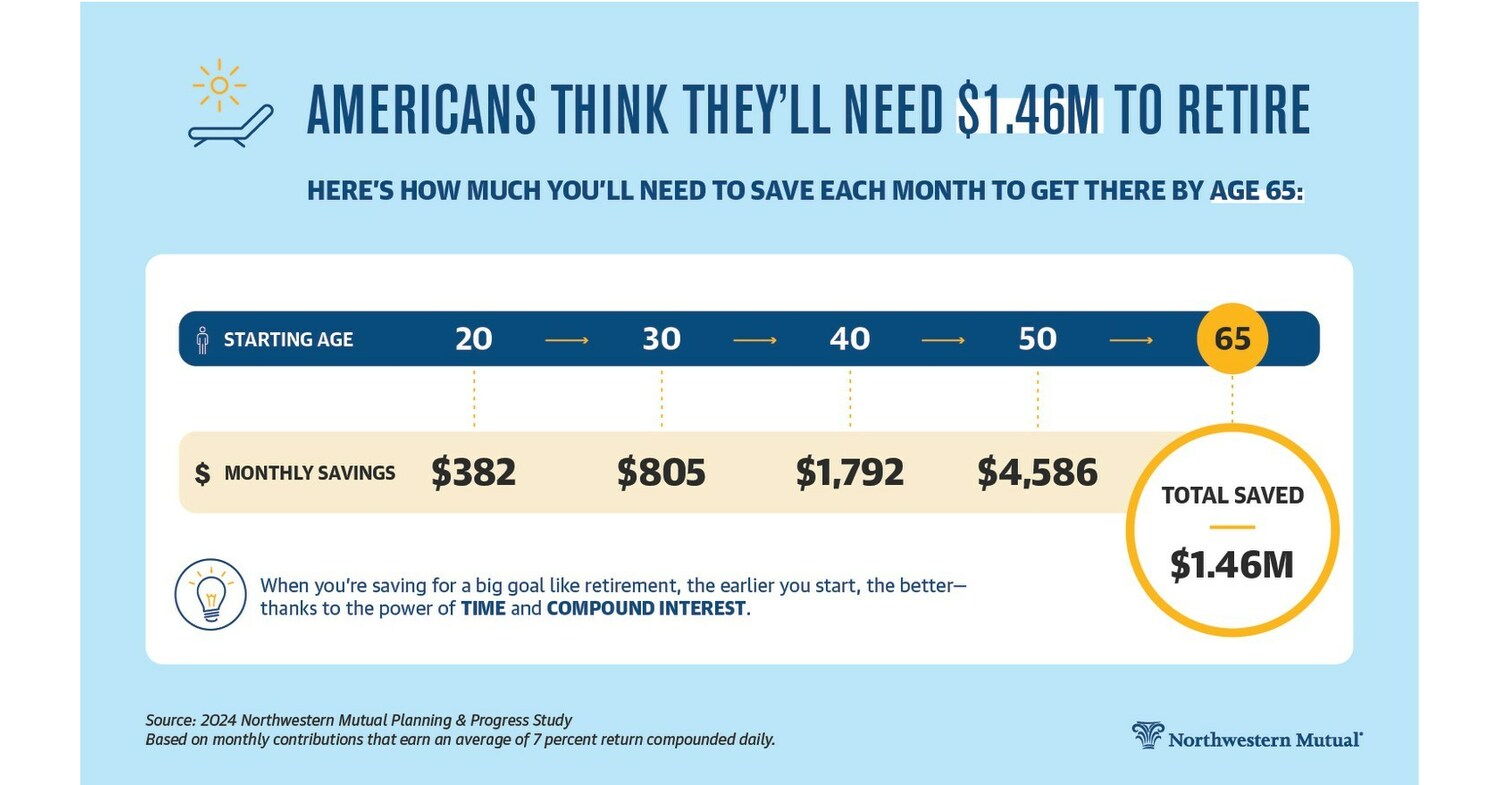

U.S. adults imagine they are going to want $1.46 million to retire comfortably, a 15% enhance over the $1.27 million reported final 12 months, far outpacing as we speak’s inflation charge which at present hovers between 2% and three%. Over a five-year span, folks’s ‘magic quantity’ has jumped a whopping 53% from the $951,000 goal Individuals reported in 2020.

|

2024 |

2023 |

2022 |

2021 |

2020 |

|

|

Quantity anticipated to |

$1.46M |

$1.27M |

$1.25M |

$1.05M |

$951K |

By technology, each Gen Z and Millennials count on to want greater than $1.6 million to retire comfortably. Excessive-net-worth people – folks with greater than $1 million in investable belongings – say they’re going to want almost $4 million.

|

2024 |

All |

Gen Z |

Millennials |

Gen X |

Boomers+ |

HNW ($1M+) |

|

Quantity anticipated to |

$1.46M |

$1.63M |

$1.65M |

$1.56M |

$990K |

$3.93M |

In the meantime, the typical quantity that U.S. adults have saved for retirement dropped modestly from $89,300 in 2023 to $88,400 as we speak, however is greater than $10,000 off its five-year peak of $98,800 in 2021.

|

2024 |

2023 |

2022 |

2021 |

2020 |

|

|

Quantity saved for retirement at present |

$88,400 |

$89,300 |

$86,900 |

$98,800 |

$87,500 |

|

Hole between retirement objective and present financial savings |

$1.37M |

$1.18M |

$1.16M |

$951K |

$864K |

“In 2023, the hovering value of eggs within the grocery retailer symbolized inflation in America. In 2024, it is nest eggs,” mentioned Aditi Javeri Gokhale, chief technique officer, president of retail investments and head of institutional investments at Northwestern Mutual. “Folks’s ‘magic quantity’ to retire comfortably has exploded to an all-time excessive, and the hole between their objectives and progress has by no means been wider. Inflation is increasing our expectations for retirement financial savings, and placing the strain on to plan and keep disciplined. Making a ‘magic quantity’ seem is not about waving a wand; it is about utilizing time-tested methods and studying from a talented advisor.”

Throughout all segments, there are massive gaps between what folks suppose they’re going to have to retire and what they’ve saved so far.

|

All |

Gen Z |

Millennials |

Gen X |

Boomers+ |

HNW ($1M+) |

|

|

Quantity saved for retirement at present |

$88,400 |

$22,800 |

$62,600 |

$108,600 |

$120,300 |

$172,100 |

|

Hole between retirement objective and present financial savings |

$1.37M |

$1.61M |

$1.59M |

$1.45M |

$870K |

$3.76M |

Gen Z: Beginning sooner with the goal of ending earlier

The research finds the typical age that Individuals say they began saving for retirement is 31. However for Gen Z, it is 22 – almost a decade earlier. It is also a full 15 years earlier than Boomers+ who say they began once they have been 37. Millennials and Gen X’ers started saving for retirement at ages 27 and 31, respectively.

The hope amongst Gen Z is that by beginning to save sooner, they’re going to be capable to retire earlier. They count on to retire on the age of 60, a dozen years earlier than Boomers+ who say they’re going to work till they’re 72. Millennials and Gen X’ers count on to work till 64 and 67, respectively. The typical age most individuals count on to work to is 65.

The analysis found that three in 10 Millennials and Gen Z Individuals imagine it is doubtless or extremely doubtless that they are going to reside to age 100. The sentiment amongst these youthful generations is stronger than older generations. Amongst Gen X and Boomers+, simply 22% and 21% respectively agreed that they believed they’d reside to 100.

“These numbers inform an interesting story concerning the profound shift in monetary planning that has taken form in America,” mentioned Javeri Gokhale. “Younger folks as we speak acknowledge the worth of retirement planning and constructing wealth early on in life and are getting a major head begin over their dad and mom and grandparents. On the similar time, Gen Z is redefining retirement and signaling that they plan to have lengthy and fulfilling post-career lives. The excellent news is that they’re investing earlier to allow them to save the cash they should take pleasure in it.”

The ‘Silver Tsunami’ is right here

In 2024, greater than 4 million Individuals will flip 65. That is a mean of 11,000 Individuals per day, and it’ll proceed by 2027. It is the biggest surge of Individuals hitting the standard retirement age in historical past.

The 2024 Planning & Progress Research discovered that amongst generations closest to retirement, simply half of Boomers+ (49%) and Gen X (48%) imagine they are going to be financially ready when the time comes.

On common, Gen X believes there’s a 42% probability they might outlive their financial savings, whereas Boomers+ put the chance at 37%. Throughout each generations, greater than a 3rd (37% and 38%, respectively) haven’t taken any steps to handle the potential of outliving their financial savings.

“The ‘Silver Tsunami’ is right here,” mentioned Javeri Gokhale. “Whereas youthful generations are centered on constructing wealth and defending what they’ve already constructed, Gen X and Boomers have a further necessary activity: paying themselves first in retirement. The place they’ve financial savings might be simply as necessary as how a lot they’ve saved. Carried out properly, a complete monetary plan can protect 1000’s of hard-earned {dollars} to fund these golden years. For anybody who isn’t positive how you can streamline and protect each penny, an skilled monetary advisor is usually a nice useful resource.”

When digging into among the most urgent challenges related to retirement planning, the analysis exhibits that Boomers+ and Gen X haven’t got markedly sturdy confidence of their preparedness.

|

Boomers+ |

Gen X |

|

|

I understand how a lot cash I might want to retire comfortably |

49 % |

40 % |

|

I’ve a plan to handle healthcare prices in retirement |

56 % |

44 % |

|

I’ve deliberate for the chance that I might outlive my financial savings |

37 % |

35 % |

|

I’ve a plan to handle long-term care wants in retirement |

41 % |

34 % |

|

I’ve deliberate for the potential that Social Safety could or could not |

39 % |

42 % |

|

I’ll have sufficient to depart behind an inheritance or reward to cherished |

50 % |

36 % |

|

I’ve a superb understanding of how taxes might affect my |

58 % |

46 % |

|

I’ve a superb understanding of how potential drops within the inventory |

58 % |

51 % |

Taxes are an afterthought

Solely three in 10 (30%) Individuals have a plan to reduce the taxes they pay on their retirement financial savings. Amongst them, the highest 10 methods employed embody:

- Making withdrawals strategically from conventional and Roth accounts to stay in a decrease tax bracket (32%)

- Utilizing a mixture of conventional and Roth retirement accounts (30%)

- Making strategic charitable donations (24%)

- Utilizing a Well being Financial savings Account (HSA) or different tax-advantaged healthcare account (23%)

- Utilizing merchandise like everlasting life insurance coverage or annuities for the tax advantages (22%)

- Making Roth conversions previous to taking RMDs or Social Safety (19%)

- Utilizing certified charitable distributions from an IRA (17%)

- Making contributions to different tax-advantaged accounts like a 529 (14%)

- Utilizing the premise paid into the money worth of everlasting life insurance coverage to stay in a decrease tax bracket (13%)

- Benefiting from a Certified Longevity Annuity Contract (QLAC) to put aside funds for later in retirement (13%)

“Placing cash right into a 401K will not be sufficient to retire comfortably if the monetary plan does not deal with the affect of taxes on retirement revenue,” mentioned Javeri Gokhale. “Most individuals do not realize that their retirement revenue could also be taxed about 20% or 30% once they withdraw and spend it. After they acknowledge the affect, it is typically too late for them to regulate. A complete monetary plan will help folks get to and thru retirement by minimizing publicity and stopping anybody from paying extra in taxes than they need to be – doubtlessly preserving 1000’s of {dollars} of their nest eggs.”

In forthcoming information units, the 2024 Planning & Progress Research will discover wide-ranging points dealing with Individuals spanning financial savings and debt, retirement revenue, rising expertise, skilled assist and extra.

About The 2024 Northwestern Mutual Planning & Progress Research

The 2024 Planning & Progress Research was carried out by The Harris Ballot on behalf of Northwestern Mutual amongst 4,588 U.S. adults aged 18 or older. The survey was carried out on-line between January 3 and January 17, 2024. Knowledge are weighted the place vital by age, gender, race/ethnicity, area, training, marital standing, family measurement, and family revenue to carry them consistent with their precise proportions within the inhabitants. An entire survey methodology is on the market.

About Northwestern Mutual

Northwestern Mutual has been serving to folks and companies obtain monetary safety for greater than 165 years. By a complete planning method, Northwestern Mutual combines the experience of its monetary professionals with a personalised digital expertise and industry-leading merchandise to assist its shoppers plan for what’s most necessary. With over $627 billion of complete belongings[i] being managed throughout the corporate’s institutional portfolio in addition to retail funding shopper portfolios, greater than $36 billion in revenues, and $2.3 trillion value of life insurance coverage safety in power, Northwestern Mutual delivers monetary safety to greater than 5 million folks with life, incapacity revenue and long-term care insurance coverage, annuities, and brokerage and advisory companies. Northwestern Mutual ranked 111 on the 2023 FORTUNE 500 and was acknowledged by FORTUNE® as one of many “World’s Most Admired” life insurance coverage corporations in 2024.

Northwestern Mutual is the advertising title for The Northwestern Mutual Life Insurance coverage Firm (NM), Milwaukee, WI (life and incapacity insurance coverage, annuities, and life insurance coverage with long-term care advantages) and its subsidiaries. Subsidiaries embody Northwestern Mutual Funding Providers, LLC (NMIS) (funding brokerage companies), broker-dealer, registered funding adviser, member FINRA and SIPC; the Northwestern Mutual Wealth Administration Firm® (NMWMC) (funding advisory and companies), federal financial savings financial institution; and Northwestern Lengthy Time period Care Insurance coverage Firm (NLTC) (long-term care insurance coverage). Not all Northwestern Mutual representatives are advisors. Solely these representatives with “Advisor” of their title or who in any other case disclose their standing as an advisor of NMWMC are credentialed as NMWMC representatives to offer funding advisory companies.

i Consists of investments and separate account belongings of Northwestern Mutual in addition to retail funding shopper belongings held or managed by Northwestern Mutual.

This materials isn’t meant as authorized or tax recommendation. Monetary Representatives don’t give authorized or tax recommendation. Taxpayers ought to confer with an impartial tax or authorized advisor

SOURCE Northwestern Mutual

{kind=link}