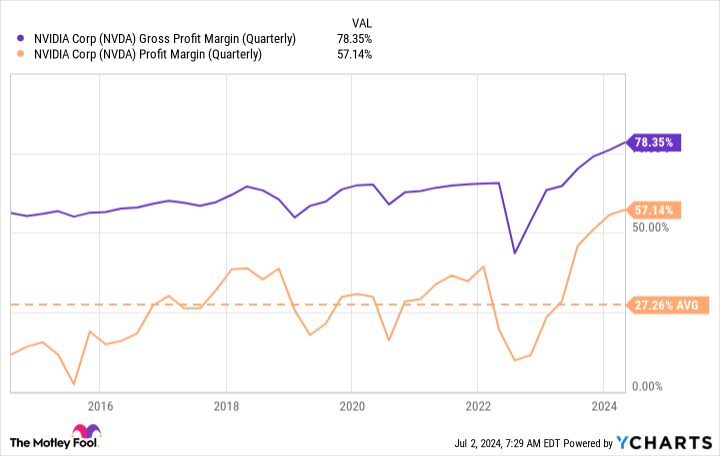

Nvidia (NASDAQ: NVDA) has accomplished rather a lot over the previous 5 years. 5 years in the past, it was nearing the underside of a cycle due to a collapse within the cryptocurrency market. Now, it is reaching new highs as its graphics processing items (GPUs) are in excessive demand for creating synthetic intelligence (AI) fashions.Whereas it could have been practically inconceivable to foretell all the locations Nvidia has gone over the previous 5 years, I will speculate on the place it might go within the subsequent 5 years. Though this prediction will probably be unsuitable in some methods, it is good at the least to develop an funding thesis for the market’s most dominant firm proper now.Nvidia’s best-in-class GPUs are about to face some competitionNvidia’s GPUs are — arms down – the most effective in school. There is a cause why all the largest firms that present the instruments to make AI fashions or create them in-house are utilizing Nvidia GPUs practically solely. Nonetheless, that exclusivity could also be dwindling.As a result of GPUs can do a number of calculations in parallel, they’re incredible for creating AI fashions. Nonetheless, if the one factor that the GPU will probably be doing is coaching AI fashions, extra environment friendly {hardware} is out there. For example, Google Cloud’s tensor processing unit (TPU) is more practical at coaching AI fashions than a GPU if the workload is ready as much as be run on a TPU.This nonetheless leaves a use case for GPUs, that are incredible for working preliminary fashions. Nonetheless, custom-designed AI chips like TPUs can exceed the efficiency of GPUs when they’re used for a particular function.Google Cloud is not the one one creating these {custom} chips. Amazon Internet Companies, Microsoft Azure, and Meta Platforms are additionally creating their very own custom-designed chips. This might current an issue for Nvidia over the subsequent 5 years, as lots of its largest prospects are bringing these designs in-house. Demand for Nvidia GPUs will nonetheless probably be excessive, nevertheless it might not be as excessive as it’s now.On the plus aspect for Nvidia, all the record-setting variety of GPUs it has bought over the previous yr will ultimately should be changed. Whereas there isn’t any onerous and quick rule, it is common for these GPUs to final between three and 5 years in a knowledge middle. After that, they will both should be changed (whether or not by some in-house design or Nvidia’s newest product) or decommissioned.The computing energy to run these fashions repeatedly is not going away, so decommissioning these GPUs is not an choice. It will create basically a long-term subscription impact, and 5 years from now, Nvidia will probably see one other wave of changing the merchandise it’s promoting proper now.Story continuesThat’s to not point out all the technological enhancements that can probably be comprised of now till then, as new chip know-how (like Taiwan Semiconductor’s 2-nanometer chip know-how that will probably be extra environment friendly than the earlier era) will create extra highly effective and environment friendly GPUs that can assist its customers out over the long term.However is all of that already baked into the inventory worth?Nvidia’s revenue margins are ripe for competitionIt’s no secret that Nvidia’s inventory is dear. The shares commerce at 73 instances trailing and 46 instances ahead earnings, which implies vital development is already priced into the inventory.Nonetheless, Nvidia’s file margins aren’t usually mentioned. Nvidia’s near-60% profit-margin ranges are unbelievable and are a major cause why many firms are beginning to design their chips in-house.NVDA Gross Revenue Margin (Quarterly) ChartBecause demand for Nvidia’s GPUs is so excessive proper now, the corporate can afford to cost a premium for its merchandise. Ultimately, that will not be the case, and its revenue margins will probably fall over the subsequent 5 years.When that occurs, its price-to-earnings (P/E) ratio will enhance as a result of earnings both rising at a slower tempo or falling. It is a large danger related to the inventory, because the market believes Nvidia’s income will preserve going straight up endlessly.Whereas demand for Nvidia’s merchandise will probably stay elevated, do not be stunned when Nvida faces challenges with in-house options within the subsequent few years. There’s an outdated saying that an organization’s margins are a competitor’s alternative, and when Nvidia’s margins attain these ranges, there’s sure to be competitors quickly.In consequence, Nvidia’s inventory might face some strain over the subsequent 5 years. This unbelievable demand increase will not final endlessly, and the chance is simply too massive for each firm to take a seat nonetheless and watch Nvidia take their cash.Don’t miss this second probability at a doubtlessly profitable opportunityEver really feel such as you missed the boat in shopping for essentially the most profitable shares? You then’ll need to hear this.On uncommon events, our knowledgeable crew of analysts points a “Double Down” inventory advice for firms that they suppose are about to pop. If you happen to’re nervous you’ve already missed your probability to speculate, now could be the most effective time to purchase earlier than it’s too late. And the numbers converse for themselves:Amazon: in case you invested $1,000 after we doubled down in 2010, you’d have $22,254!*Apple: in case you invested $1,000 after we doubled down in 2008, you’d have $41,863!*Netflix: in case you invested $1,000 after we doubled down in 2004, you’d have $368,072!*Proper now, we’re issuing “Double Down” alerts for 3 unimaginable firms, and there might not be one other probability like this anytime quickly.See 3 “Double Down” shares »*Inventory Advisor returns as of July 2, 2024Suzanne Frey, an govt at Alphabet, is a member of The Motley Idiot’s board of administrators. John Mackey, former CEO of Complete Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Randi Zuckerberg, a former director of market improvement and spokeswoman for Fb and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. Keithen Drury has positions in Alphabet, Amazon, Meta Platforms, and Taiwan Semiconductor Manufacturing. The Motley Idiot has positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Idiot recommends the next choices: lengthy January 2026 $395 calls on Microsoft and quick January 2026 $405 calls on Microsoft. The Motley Idiot has a disclosure coverage.The place Will Nvidia Inventory Be in 5 Years? was initially printed by The Motley Idiot

The place Will Nvidia Inventory Be in 5 Years?

- Trending

- Comments

- Latest

{kind=link}